Search Options Trading Mastery:

- Home

- Advanced Strategies

- Delta Neutral Trading

Delta Neutral Trading Options Strategies

To understand how delta neutral trading works, we first need to grasp what the options delta is. When calculating an options price, we use 5 components called "the greeks".

The delta is one of these 'greeks' and simply put, is an indication of the amount by which an option price is expected to move in proportion to a price movement in the underlying financial instrument such as a company stock. It is usually expressed as a number to 4 decimal points.

Call options always have a positive delta, which may vary from virtually zero to as high as 1.0. Put options always have a negative delta with the same parameters as calls.

When an option 'strike price' is the same as the current stock price, it is called "at the money". At-the-money call and put options theoretically have a delta of 0.5 and -0.5 respectively - which means that for each point the underlying moves, the option price will initially move at half the same rate.

But the further in-the-money an option goes, the greater the delta, up to a maximum of 1.0. This effectively means that as the option price becomes profitable, it does so at an accelerating rate.

So let's imagine we were looking at some options with a strike (exercise) price of $100 and then compared this to various prices at which the underlying stock might trade. We notice the following:

Stock price is at $85 - CALL options will be 'out of the money' and have a delta of 0.0148

Stock price is at $85 - PUT options will be 'in the money' and have a delta of -0.9852

The total of the above two deltas (ignoring negative and positive) equals 1.0000

If we held both positions, they would be delta neutral.

So when the stock price is at $85, the value of a put option contract with a strike price of $100 would increase at almost a 1:1 ratio with the underlying if the stock price continues to fall below $85. The way-out-of-the-money $100 call option however, would hardly move in value at all.

So the delta is a measure of the SENSITIVITY of option prices to the price movements in the underlying.

Delta Neutral Trading in Action

1. Hedging Your Share Portfolio

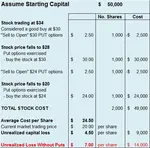

Let's say we own 200 shares currently trading at $110. We want to hedge our shares against future loss, but also in such a way that we can profit from a rise in share price as well.

We observe the options delta for $110 put options is -0.4200 and they cost $0.91 each. We also note from today's list of options prices, that should the share price rise to $112, our put options will decrease in value to $0.28 each with a delta of -0.16.

The 'delta' of the company shares themselves will of course, be 1.0000

Our 200 shares have a total delta of 2.0000 (2 x 1.0000)

We need to purchase 5 x $110 put option contracts at a delta of -0.42 to give us a total delta of -2.10 (5 x -0.42)

Our overall position delta is therefore -0.10 (2.0000 - 2.1000)

Scenario 1: The Stock Price Increases

Should the share price now increase to $112, our put options will decrease in value to $0.28 and our loss will be $0.63 per contract, or $315 total (0.63 x 100 x 5)

Our shares however, will increase in value by $400 (200 x $2)

So our overall net profit 'on paper' will be $85 (400 - 315) or $0.425 per share.

Scenario 2: The Stock Price Falls

If the share price now falls by $2 to $108, our put options will be 'in the money' and increase in value to $2.14 with a delta of -0.73 and realize a profit of $1.23 per contract, or $615 total (1.23 x 100 x 5)

Our loss on shares however, will be $400 (200 x $2)

So our overall net profit will be $215 or $1.075 per share.

These two scenarios work on the assumption that the underlying price movements will be in the short term and do not take into account the time decay factor in option pricing.

Nevertheless, all the information you need for delta neutral trading can be obtained from looking at the option chains data on any reputable broker site.

Once you understand how delta neutral trading works, why limit yourself to hedging shares? Instead of risking $22,000 on 200 shares at $110, why not set up the same position for a fraction of the cost using futures contracts or a 'synthetic stock position' (buying calls and selling puts at the same strike price) instead of buying the shares themselves?

Futures contracts and synthetic stock positions have a 1.0000 delta with the underlying, so you can receive the same outcomes and put your funds to better use elsewhere.

You can do the same thing with currency options using the leveraged spot price for forex pairs.

Delta Neutral Trading with Options

Straddles and Strangles

The straddle is the classic and most widely known delta neutral option trading strategy. A straddle is defined by the purchase of an equal number of at-the-money (ATM) call and put options with the same expiration date.

Since ATM options have a delta of around 0.5000 and since calls are positive and put deltas are always negative, the one will balance out the other to make the overall position 'delta neutral'.

Strangles on the other hand, involve OTM options whose deltas will be much less than 0.5 or -0.5. But again, depending on the price of the underlying financial instrument in relation to the option strike prices when you buy, the respective OTM deltas should practically neutralise each other.

Excellent profits can be made from delta neutral trading using options alone, but you must take other other 'greeks' particularly theta (time decay) into account when choosing your positions.

Straddles and Share Transactions - Gamma Scalping

Once you understand how delta neutral trading really works, you can use it to profit from straddle trades another way. In our example above, we used the delta to determine how many option contracts we would need to purchase to hedge the shares we own.

But we can also do it the other way around. If we start with a straddle in place, we can use the delta for various strike prices to determine how many shares we would need to buy or sell in order to remain delta neutral.

Remember, stock prices always have a delta of 1:1 while options don't. We can take advantage of this knowledge and use straddles combined with going long or short shares to 'scalp' profits in a day trading strategy. You can learn more about this in module 11 video files that come with the popular Trading Pro System.

Other Considerations

When assessing the viability of a delta neutral trade, you should also be aware of an associated 'greek' called the Gamma. The GAMMA is the rate at which the DELTA changes in response to price movements in the underlying. It is the factor that causes a delta to change from -0.5 for an ATM put option, to -0.74 as it goes further into the money.

Using a good option pricing model, you can use the gamma to calculate the theoretical delta and therefore the theoretical future price of an option, in response to price movements in the underlying. This is particularly useful if you are using options for delta neutral trading alongside futures or synthetic stock positions.

Enjoy This Video About Delta Neutral Trading

**************** ****************

Return to Option Trading Strategies Contents Page

Go to Option Trading Homepage

Popular Articles

-

Near Riskless Trading Strategies

Near Riskless Trading strategies using options, allows you to use advanced arbitrage techniques for highly profitable, almost risk free results. -

Wealth Building Options Trading

Wealth building options trading - how to profit from share investments even if you buy at the top of the market.

Wealth building options trading - how to profit from share investments even if you buy at the top of the market. -

The Three Legged Box Spread - A Great Lifestyle Trade

Whether you only have a few thousand or a large sum to invest, the Three Legged Box Spread is one of the best option trading strategies available for retail investors today.

Whether you only have a few thousand or a large sum to invest, the Three Legged Box Spread is one of the best option trading strategies available for retail investors today. -

XTR ProTrader Signals

-

The Double Calendar Spread

The double calendar spread is a very safe option strategy which profits consistently - provided you know exactly what to do when price action threatens it.

The double calendar spread is a very safe option strategy which profits consistently - provided you know exactly what to do when price action threatens it. -

ETF Options - Why You Should Trade Them

ETF Options when combined with the right options strategy, can be one of the best and safest ways to profit consistently from the financial markets.

ETF Options when combined with the right options strategy, can be one of the best and safest ways to profit consistently from the financial markets. -

The Covered Put Option Strategy

The covered put option strategy explained, with payoff diagram and examples. These are most suited to a bearish to neutral market.

The covered put option strategy explained, with payoff diagram and examples. These are most suited to a bearish to neutral market. -

How to Use the VIX

Knowing how to use the VIX should be essential for all traders whose portfolio of positions may be affected by general market sentiment.

Knowing how to use the VIX should be essential for all traders whose portfolio of positions may be affected by general market sentiment. -

Using Options to Buy Stocks at Discount Prices

Did you know that you could be using options to buy stocks so much cheaper than if you just went to your broker and simply bought them at market price?

Did you know that you could be using options to buy stocks so much cheaper than if you just went to your broker and simply bought them at market price? -

How Option Price Movements Effect Gains and Losses

Knowing about and understanding how options work is a potent arrow in a trader’s quiver. One of the things that people new to options must understand -

When can you trade Forex Options?

The forex market is the largest financial market in the world which works 24 hours, 5 days per week, if you consider the whole world as a single entity. -

Iron Condor Option Strategy

In this iron condor option strategy we show you the best way to leg into positions safely and also to adjust your positions when they are threatened.

In this iron condor option strategy we show you the best way to leg into positions safely and also to adjust your positions when they are threatened. -

What is a Straddle Option? A Great Delta Neutral Strategy!

So what is a straddle option and why is it such a great options trading strategy? You don't have to pick market direction and can still profit very well.

So what is a straddle option and why is it such a great options trading strategy? You don't have to pick market direction and can still profit very well. -

The Long Iron Butterfly - Credit Spreads on Steroids

The long iron butterfly is a range trading strategy and a variation of the Iron Condor. Both these strategies use two credit spreads using both calls and puts

The long iron butterfly is a range trading strategy and a variation of the Iron Condor. Both these strategies use two credit spreads using both calls and puts -

The Distinct Advantage Credit Spreads Are Known For

So what is the advantage credit spreads give us? This example will demonstrate how we can turn a losing trade into a profitable one.

So what is the advantage credit spreads give us? This example will demonstrate how we can turn a losing trade into a profitable one. -

Box spreads Illustrated and Explained

Box spreads are an option trading strategy that involves purchasing a bull-call spread with a corresponding bear-put spread. The two vertical spreads have the same expiration dates and strike prices. -

Exotic Options Explained With Examples

Exotic options are typically more complex than regular options. They are most popularly traded on currency pairs but can also be traded on stock options, stock indexes, warrants and commodity options -

Hoadley Options Tools Review

Hoadley Options Trading and Investment Tools is an Excel based tool that makes options risk analysis easy.

Hoadley Options Trading and Investment Tools is an Excel based tool that makes options risk analysis easy. -

Free Option Trading Software

So we've done some research for you and below, you'll find a summary of some of the best free option trading software available. -

Invest in Soxange and Multiply Earnings through Copying the Top Traders in this Social Network

Within the context of the online trading world, SoXange is one of the few trading platforms that draw all kinds of traders in droves to that online trading

Amazon Affiliate

Copyright © 2002- Options Trading Mastery. ALL RIGHTS RESERVED.

Other Recommended sites:

NaturalRelieved | European Travel Escape | Relationships Guide

New! Comments

Have your say about what you just read! Leave me a comment in the box below.