Search Options Trading Mastery:

- Home

- Explain Option Trading

- Options Greeks

The Option Greeks Explained

Option Greeks - The Key to Making the Best Option Strategies Work

The Option Greeks are a selection of five Greek letters which have been chosen to represent the components that make up the calculation of the price of an option contract at any given time. Once you start trading stocks and options, you're going to want to know everything about what affects the price of an option.

Whether you're going "long" or "short" with options, understanding these components will help you to make profitable decisions.

There is much more to the value of an option contract than the strike price, expiration date and in-the-money value. Have you ever wondered for example, why you bought an option, then the price of the underlying then moved in your favor and yet the option value didn't increase?

You can blame the Option Greeks for that!

The Option Greeks include the following variables:- The delta, the gamma, the theta, the vega and rho.

So let's take a look at what each of these mean and how they affect an option's value.

Option Greeks - The Delta

The Delta is a measure of a change in the option's value in relation to a one point move in the price of the underlying - whether that's a stock, a future, an index or an ETF.

Long Call options and short put options always have positive delta while long puts and short calls always have negative delta.

So let's say we had a position with a delta of -20. This means that if the price of the underlying increased by one dollar, we would lose $20 on the value of either our "long" put options position or our "short" call options position.

You could think of the delta as an alternative to owning the underlying stock. If you were "short" the stock, you would make a $20 profit if the stock price went down by one dollar. Understanding this principle can help you to adjust your positions if you want to remain "delta neutral".

If you have a portfolio of option positions, your total (or 'net') delta number will reveal how sensitive your positions are to an overall move in the underlying stocks behind your options portfolio. So theoretically, with a total delta of say -27, we would gain $27 if the overall market were to decline by one point.

But what if your net delta was -300 and the market was experiencing an upward rally? What would you need to do in order to adjust your positions?

Option Greeks - The Gamma

The Gamma is the measure of the rate of change of an option's delta with respect to a one point move in the underlying stock. It affects the option's delta more than the price of the option itself.

When you buy an option, gamma is positive and when selling (going short) an option, gamma is negative, regardless of whether it's a call or put. In practical terms, you would be looking for a positive gamma if you believe the underlying is about to make a large move.

Going "long" calls and puts gives a positive gamma and you make more money when the market moves, so this would ideally suit an options straddle position.

But if you're "short" calls or puts, you will be negative gamma and that means that you don't want the market to move too much in order to stay profitable.

Option strategies such as credit spreads and iron condors are examples of negative gamma positions.

Option Greeks - Theta

When your postitions are "short" you will have negative gamma, but this means you're also going to be positive theta. Theta is the measure of how much an option loses its value on a daily basis as the expiration date approaches.

Theta increases exponentially the closer you get to expiration.

For long positions, theta tells you how many dollars you lose each day while the underlying price action goes nowhere. This is why simple long positions need to not only be correct with regard to direction but also timing.

For short positions, the Theta number you see in your options position statement tells you the number of dollars profit you receive each day until expiration, providing the underlying remains out-of-the-money (OTM). This dollar amount will increase each day and especially so during expiration week.

Knowing how to read the theta in connection with the other "greeks" so that you know when it's necessary to adjust your positions, is the key to making a profit with "short" options positions.

This is covered more fully in the Trading Pro System video series.

Option Greeks - Vega

The Vega is one of the most important components that affect the price of an option. It is the most powerful of all the "Greeks".

Vega measures the amount an option will change in value after a one point change in volatility. If our vega number is positive then aside from the implications behind the other Greeks, we will gain an additional profit for every one point increase in the volatility of the market.

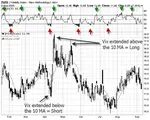

Vega is measured by the volatility index of the Chicago Board Options Exchange (CBOE), whose symbol in the USA is the $VIX. It is determined by the number of put options being purchased on the CBOE. Put option purchases are an indication of market fear that prices are about to fall.

Analyzing a chart of the $VIX should be an important feature of your option strategies, as the popular Trading Pro System structured options training program clearly describes. The video at the beginning of this article has been taken from that options course.

When the $VIX index goes up, stock prices normally go down and vice versa. Just compare a chart of the $VIX with the Dow Jones Index sometime and you'll see the connection.

If our vega is positive, we make additional money if underlying prices go down. So if our theta number is positive and becomes too large, we are vulnerable to any further upward moves in the market. So you should try to keep it as neutral as possible.

Option Greeks - Rho

Rho is about how much an option price changes in value as a result of a one point change in interest rates. The theory is that when you invest in options, you are sacrificing money that could otherwise be sitting in an account earning interest.

As such, it is not a significant factor.

All things being equal, we prefer delta and vega to be relatively neutral. Option strategies involving going long and short both calls and puts creates this initial neutrality.

If you would like more information on how you can use the Greeks to create and adjust positions in connection with specific strategies, for low stress consistent profits, then take a look at the Options Trading Pro System - 24 hours of comprehensive video options trading training.

**************** ****************

Return to Explain Option Trading Contents Page

Go to Option Trading Homepage

Add a Comment

We and other readers of this information site value your input.

You can also (optionally) include any graphics such as charts, if you wish.

Popular Articles

-

Near Riskless Trading Strategies

Near Riskless Trading strategies using options, allows you to use advanced arbitrage techniques for highly profitable, almost risk free results. -

Wealth Building Options Trading

Wealth building options trading - how to profit from share investments even if you buy at the top of the market.

Wealth building options trading - how to profit from share investments even if you buy at the top of the market. -

The Three Legged Box Spread - A Great Lifestyle Trade

Whether you only have a few thousand or a large sum to invest, the Three Legged Box Spread is one of the best option trading strategies available today.

Whether you only have a few thousand or a large sum to invest, the Three Legged Box Spread is one of the best option trading strategies available today. -

XTR ProTrader Signals

-

The Double Calendar Spread

The double calendar spread is a very safe option strategy which profits consistently - provided you know exactly what to do when price action threatens it.

The double calendar spread is a very safe option strategy which profits consistently - provided you know exactly what to do when price action threatens it. -

ETF Options - Why You Should Trade Them

ETF Options when combined with the right options strategy, can be one of the best and safest ways to profit consistently from the financial markets.

ETF Options when combined with the right options strategy, can be one of the best and safest ways to profit consistently from the financial markets. -

The Covered Put Option Strategy

The covered put option strategy explained, with payoff diagram and examples. These are most suited to a bearish to neutral market.

The covered put option strategy explained, with payoff diagram and examples. These are most suited to a bearish to neutral market. -

How to Use the VIX

Knowing how to use the VIX should be essential for all traders whose portfolio of positions may be affected by general market sentiment.

Knowing how to use the VIX should be essential for all traders whose portfolio of positions may be affected by general market sentiment. -

Using Options to Buy Stocks at Discount Prices

Did you know that you could be using options to buy stocks so much cheaper than if you just went to your broker and simply bought them at market price?

Did you know that you could be using options to buy stocks so much cheaper than if you just went to your broker and simply bought them at market price? -

How Option Price Movements Effect Gains and Losses

Knowing about and understanding how options work is a potent arrow in a trader’s quiver. One of the things that people new to options must understand -

When can you trade Forex Options?

The forex market is the largest financial market in the world which works 24 hours, 5 days per week, if you consider the whole world as a single entity. -

Iron Condor Option Strategy

In this iron condor option strategy we show you the best way to leg into positions safely and also to adjust your positions when they are threatened.

In this iron condor option strategy we show you the best way to leg into positions safely and also to adjust your positions when they are threatened. -

What is a Straddle Option? A Great Delta Neutral Strategy!

So what is a straddle option and why is it such a great options trading strategy? You don't have to pick market direction and can still profit very well.

So what is a straddle option and why is it such a great options trading strategy? You don't have to pick market direction and can still profit very well. -

The Long Iron Butterfly - Credit Spreads on Steroids

The long iron butterfly is a range trading strategy and a variation of the Iron Condor. Both these strategies use two credit spreads using both calls and puts -

The Distinct Advantage Credit Spreads Are Known For

So what is the advantage credit spreads give us? This example will demonstrate how we can turn a losing trade into a profitable one. -

Box spreads Illustrated and Explained

Box spreads are an option trading strategy that involves purchasing a bull-call spread with a corresponding bear-put spread. The two vertical spreads have the same expiration dates and strike prices. -

Exotic Options Explained With Examples

Exotic options are typically more complex than regular options. They are most popularly traded on currency pairs but can also be traded on stock options, stock indexes, warrants and commodity options -

Hoadley Options Tools Review

Hoadley Options Trading and Investment Tools is an Excel based tool that makes options risk analysis easy.

Hoadley Options Trading and Investment Tools is an Excel based tool that makes options risk analysis easy. -

Free Option Trading Software

So we've done some research for you and below, you'll find a summary of some of the best free option trading software available. -

Invest in Soxange and Multiply Earnings through Copying the Top Traders in this Social Network

Within the context of the online trading world, SoXange is one of the few trading platforms that draw all kinds of traders in droves to that online trading

{kind=link}

Amazon Affiliate

Copyright © 2002- Options Trading Mastery. ALL RIGHTS RESERVED.

Other Recommended sites:

NaturalRelieved | European Travel Escape | Relationships Guide

New! Comments

Have your say about what you just read! Leave me a comment in the box below.