Search Options Trading Mastery:

- Home

- Option Spread Trading

- Call Ratio Backspread

Call Ratio Backspread

The call ratio backspread is a bullish options strategy and the reverse of the ratio call spread. Whereas a standard ratio spread seeks to profit from neutral market conditions, backspreads are best suited to a volatile market. What defines them as backspreads, is that you're selling in-the-money calls and purchasing cheaper out-of-the-money calls.

We could summarize the differences this way:

A call spread is a debit spread with equal number of option contracts at each strike price.

A call backspread is simply a credit spread with equal number of option contracts at each strike price.

A call ratio backspread is structured the same way as a credit spread, except that you're buying more OTM options than the ITM options that you're selling. This means that you sell a lesser number of calls at a lower strike price and buy more at a higher strike price.

Below is a typical 1:2 ratio construction example, but you can vary it by trying other ratios such as 2:3 or 3:5 depending on the implied volatility in the option strikes that you're using.

| Call Ratio Backspread Setup |

| Sell 1 ITM Call Buy 2 OTM Calls |

Call Ratio Backspread - Advantages and Disadvantages

The appealing thing about this strategy, is that it involves limited downside risk when compared to just buying calls, but unlimited potential profit to the upside. Placing these trades on strong, uptrending stocks will increase your chances of success.

Another advantage is the cost. Since this is a bullish strategy and your aim should be to put these on for a credit, the cost of entry is less than buying a long call.

If held until expiration date, under a 1:2 ratio a profit will be observed when the trading price of the underlying is greater than or equal to, two times the difference between the strike prices of the short and long calls, plus the net premium received, if applicable.

Because you're relying on a significant move in the price of the underlying in order to profit, the call ratio backspread is best put on using options with about 180 days to expiration.

This gives it time to do its work, as it is unlikely that any stock or ETF will remain within a tight range over a 6 month period. It is for this reason that some have called them "vacation spreads" because you can literally take a holiday and come back later to take a profit.

Breakeven Points

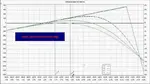

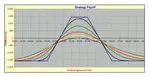

Looking at the risk graph below, you'll notice that there are 2 breakeven points. The upper and lower breakevens (at expiration) are the strike prices of the short and long calls.

Call Ratio Backspread - Example

Let's say we're looking at a chart of a given stock in March and notice that over time, the price has fallen to what we believe is a support level.

We want to take advantage of a potential price reversal at a time when OTM call options have a lower implied volatility than ITM calls. The current stock price is $43 but we believe that within 6 months, it could easily return to it's previous high of $60.

So here's what we do:

1. Sell 1 ITM October calls with $40 strike

2. Buy 2 OTM October calls with $45 strike

The position is entered for zero cost.

Looking at our payoff diagram below, the following scenarios then apply.

Let's say that at expiration date in October (7 months away) the stock price hasn't done much and is now trading at $45. The $40 sold calls will be $5 in the money while the $45 calls will be at the money.

In this scenario, we realize our maximum loss of $500. If we were able to realize an initial credit upon entry due to a reverse volatility skew, this credit would offset the maximum loss.

However, should the stock rally to $50 at expiration date, all options positions will be in the money. The $40 options will have $10 intrinsic value while the $45 options will have $5 intrinsic value. Since we own twice as many $45 options as we sold, we will break even. If we received a credit upon entry, we will take a small profit.

Beyond the $50 mark, our position begins to make a profit. So if we reached our target of $60 in 7 months time, our profit will be $1,000 less commissions, plus any intial credit received, if applicable.

But what if the stock price should continue falling? Should this happen, we will suffer no loss because it cost us nothing to enter the position. Using varying ratios, particularly a 0.67 ratio (Sell 2: Buy 3), we can usually bring in an initial credit so that should the stock price move south instead of north, we will actually make a small profit, being our initial credit.

This is where the call ratio backspread is superior to buying simple long call positions if we have a bullish view.

**************** ****************

Return to Option Spread Trading Contents Page

Go to Option Trading Homepage

Popular Articles

-

Near Riskless Trading Strategies

Near Riskless Trading strategies using options, allows you to use advanced arbitrage techniques for highly profitable, almost risk free results. -

Wealth Building Options Trading

Wealth building options trading - how to profit from share investments even if you buy at the top of the market.

Wealth building options trading - how to profit from share investments even if you buy at the top of the market. -

The Three Legged Box Spread - A Great Lifestyle Trade

Whether you only have a few thousand or a large sum to invest, the Three Legged Box Spread is one of the best option trading strategies available for retail investors today.

Whether you only have a few thousand or a large sum to invest, the Three Legged Box Spread is one of the best option trading strategies available for retail investors today. -

XTR ProTrader Signals

-

The Double Calendar Spread

The double calendar spread is a very safe option strategy which profits consistently - provided you know exactly what to do when price action threatens it.

The double calendar spread is a very safe option strategy which profits consistently - provided you know exactly what to do when price action threatens it. -

ETF Options - Why You Should Trade Them

ETF Options when combined with the right options strategy, can be one of the best and safest ways to profit consistently from the financial markets.

ETF Options when combined with the right options strategy, can be one of the best and safest ways to profit consistently from the financial markets. -

The Covered Put Option Strategy

The covered put option strategy explained, with payoff diagram and examples. These are most suited to a bearish to neutral market.

The covered put option strategy explained, with payoff diagram and examples. These are most suited to a bearish to neutral market. -

How to Use the VIX

Knowing how to use the VIX should be essential for all traders whose portfolio of positions may be affected by general market sentiment.

Knowing how to use the VIX should be essential for all traders whose portfolio of positions may be affected by general market sentiment. -

Using Options to Buy Stocks at Discount Prices

Did you know that you could be using options to buy stocks so much cheaper than if you just went to your broker and simply bought them at market price?

Did you know that you could be using options to buy stocks so much cheaper than if you just went to your broker and simply bought them at market price? -

How Option Price Movements Effect Gains and Losses

Knowing about and understanding how options work is a potent arrow in a trader’s quiver. One of the things that people new to options must understand -

When can you trade Forex Options?

The forex market is the largest financial market in the world which works 24 hours, 5 days per week, if you consider the whole world as a single entity. -

Iron Condor Option Strategy

In this iron condor option strategy we show you the best way to leg into positions safely and also to adjust your positions when they are threatened.

In this iron condor option strategy we show you the best way to leg into positions safely and also to adjust your positions when they are threatened. -

What is a Straddle Option? A Great Delta Neutral Strategy!

So what is a straddle option and why is it such a great options trading strategy? You don't have to pick market direction and can still profit very well.

So what is a straddle option and why is it such a great options trading strategy? You don't have to pick market direction and can still profit very well. -

The Long Iron Butterfly - Credit Spreads on Steroids

The long iron butterfly is a range trading strategy and a variation of the Iron Condor. Both these strategies use two credit spreads using both calls and puts

The long iron butterfly is a range trading strategy and a variation of the Iron Condor. Both these strategies use two credit spreads using both calls and puts -

The Distinct Advantage Credit Spreads Are Known For

So what is the advantage credit spreads give us? This example will demonstrate how we can turn a losing trade into a profitable one.

So what is the advantage credit spreads give us? This example will demonstrate how we can turn a losing trade into a profitable one. -

Box spreads Illustrated and Explained

Box spreads are an option trading strategy that involves purchasing a bull-call spread with a corresponding bear-put spread. The two vertical spreads have the same expiration dates and strike prices. -

Exotic Options Explained With Examples

Exotic options are typically more complex than regular options. They are most popularly traded on currency pairs but can also be traded on stock options, stock indexes, warrants and commodity options -

Hoadley Options Tools Review

Hoadley Options Trading and Investment Tools is an Excel based tool that makes options risk analysis easy.

Hoadley Options Trading and Investment Tools is an Excel based tool that makes options risk analysis easy. -

Free Option Trading Software

So we've done some research for you and below, you'll find a summary of some of the best free option trading software available. -

Invest in Soxange and Multiply Earnings through Copying the Top Traders in this Social Network

Within the context of the online trading world, SoXange is one of the few trading platforms that draw all kinds of traders in droves to that online trading

Amazon Affiliate

Copyright © 2002- Options Trading Mastery. ALL RIGHTS RESERVED.

Other Recommended sites:

NaturalRelieved | European Travel Escape | Relationships Guide

New! Comments

Have your say about what you just read! Leave me a comment in the box below.